A Guide to What Families Should Know When Cremation Planning

Last Updated: April 2026 | Reviewed for accuracy against current FTC guidelines and state Medicaid regulations

If you or a spouse is approaching Medicaid eligibility — or already receiving Medicaid long-term care benefits — the way you prepay for funeral arrangements matters enormously. The type of preneed funeral contract you choose can mean the difference between those funds being counted as a personal asset (and potentially disqualifying you from Medicaid) or being fully excluded from the asset calculation.

This guide explains how preneed funeral contracts interact with Medicaid spend-down planning, what an irrevocable funeral trust actually does, and what to verify before you sign anything. Because the rules vary significantly from state to state, we also flag the key variations you need to check in your specific state.

One area that often causes confusion is funeral planning and Medicaid eligibility. Many states allow certain funeral arrangements—such as prepaid funeral plans or funeral trusts—to be treated as exempt assets, meaning they do not count against Medicaid financial limits.

Understanding how these rules work can help families ensure funeral expenses are covered while also protecting eligibility for long-term care benefits.

Note: This article is an informational resource. For advice specific to your situation, consult a qualified elder law attorney before entering any preneed funeral contract for Medicaid planning purposes.

What Medicaid Asset Limits Mean

Eligibility for Medicaid is based partly on financial need. In most states, individuals applying for Medicaid long-term care benefits must have very limited financial resources.

Typical asset limits include:

| 👥 Applicant Type | 📊 Typical Asset Limit |

|---|---|

| Individual applicant | About $2,000 |

| Married couple (one spouse applying) | Varies by state |

Countable assets generally include:

- Bank accounts

- Investment accounts

- Cash savings

- Certain life insurance policies

- Property other than a primary residence

Because these limits are so low, many families must legally reduce their assets through a process known as spending down before Medicaid eligibility begins.

Medicaid Spend-Down Rules

The Medicaid spend-down process allows applicants to use excess assets on certain approved expenses before qualifying for benefits.

Common spend-down expenses may include:

- Medical bills

- Nursing home costs

- Home modifications for disability

- Legal and financial planning

- Funeral and burial arrangements

Planning for funeral expenses is often one of the most practical ways to legally reduce countable assets while also ensuring future funeral costs are covered.

However, Medicaid rules generally require that these arrangements be properly structured to qualify as exempt assets.

Preplanning vs. Prepaying: The Distinction That Matters Here

Before going further, it’s worth separating two concepts that are often used interchangeably but describe very different levels of commitment.

Preplanning means documenting your funeral wishes — what type of service you want, burial or cremation, music preferences, designated pallbearers — and sharing those instructions with your family. No money changes hands, and no legal obligations are created. Preplanning has no impact on Medicaid eligibility whatsoever.

Prepaying means entering a legal contract with a funeral provider and funding it now. The money leaves your control (or is supposed to), and both you and the provider take on legal obligations. It is prepaying — specifically, prepaying through an irrevocable contract — that can affect Medicaid eligibility, either to your benefit or your detriment.

For Medicaid purposes, only funded, irrevocable arrangements are relevant. The rest of this article addresses prepaid contracts specifically.

What Is a Funeral Trust?

A funeral trust is a financial arrangement that sets aside funds to pay for future funeral or burial expenses.

Funeral trusts are commonly used in funeral pre-planning and may be established through:

- Funeral homes

- Banks or financial institutions

- Insurance companies offering preneed funeral policies

The funds are typically designated to pay for services such as:

- Cremation or burial

- Funeral services

- Transportation of the deceased

- Cemetery plots or burial spaces

- Urns, caskets, or other funeral merchandise

Because the funds are earmarked specifically for funeral expenses, certain types of funeral trusts may be exempt from Medicaid asset calculations.

Revocable vs. Irrevocable Preneed Contracts: The Core Distinction

This is the single most important concept in this entire article. Most people researching preneed contracts don’t realize there are two fundamentally different types, with opposite implications for Medicaid.

Revocable Preneed Contracts

A revocable preneed contract is one you can cancel at any time and receive a refund of your funds (subject to any cancellation fees permitted by your state). Because you retain the right to access those funds, Medicaid treats the contract balance as a countable asset — just like a bank account. It counts against your eligibility limit dollar for dollar.

Revocable contracts offer more flexibility, but they offer no Medicaid planning benefit.

Irrevocable Preneed Contracts

An irrevocable preneed contract is one you permanently relinquish the right to cancel or cash out. Once funded, the money is no longer considered yours for Medicaid purposes. Federal Medicaid guidelines generally do not count an irrevocable preneed funeral contract as a personal asset, which means those funds are shielded from the Medicaid spend-down calculation.

This is the arrangement that serves a Medicaid planning purpose — but it comes with trade-offs. You lose access to those funds entirely. If your wishes change, your options are limited. And the contract must still be structured correctly to qualify under your state’s rules.

How an Irrevocable Funeral Trust Works

An irrevocable funeral trust (IFT) is one of the most common vehicles for funding an irrevocable preneed contract. Here’s how it works in practice:

- You enter a preneed contract with a licensed funeral provider, selecting the specific services and merchandise you want.

- You fund the contract by placing money into a trust administered by a third-party trustee — typically a bank or trust company.

- The trust is designated as irrevocable. You give up your right to withdraw or redirect those funds.

- When you pass away, the trustee releases funds directly to the funeral provider to fulfill the contract terms. Any remainder — funds left over after all contracted services are paid — goes to the state Medicaid program, not to your heirs (more on this below).

The key Medicaid protection comes from step 3: because you can no longer access the funds, Medicaid does not count them as your asset.

The Residual Beneficiary Requirement

This surprises many families and is worth understanding clearly before you sign. In states that allow irrevocable funeral trusts for Medicaid spend-down purposes, most require that the state Medicaid agency be named as the residual beneficiary of any funds left in the trust after funeral costs are paid.

In plain terms: if you prepay $8,000 for services that ultimately cost $6,500, the remaining $1,500 goes back to the state — not to your family. This is called Medicaid estate recovery, and it applies to the funeral trust specifically because those funds were excluded from your countable assets precisely so you could receive Medicaid benefits.

This doesn’t mean an irrevocable funeral trust is a bad deal. It simply means you shouldn’t over-fund it with the expectation that leftover money will pass to heirs. Fund it to cover your actual anticipated costs, not as a savings vehicle.

What Medicaid Excludes: Burial Space and Funeral Costs

Federal Medicaid guidelines allow two distinct categories of funeral-related exclusions, and it’s important to understand them separately because they work differently.

Burial Space Exclusions

Medicaid excludes the value of burial spaces from countable assets with no dollar limit. Burial spaces include cemetery plots, crypts, mausoleums, urns, niches, and the vaults or grave liners that many cemeteries require. This exclusion applies not just to the Medicaid applicant and their spouse, but also to their immediate family members — children, siblings, parents, and the spouses of those relatives.

This is an underutilized planning tool. A family can purchase cemetery spaces for multiple family members and exclude the full value from the Medicaid asset calculation, with no cap. The purchase must be made separately from a funeral or burial trust — it cannot be bundled into the same irrevocable contract. Ask the cemetery for a separate itemized receipt for the burial space.

Funeral Service Cost Exclusions

The exclusion for funeral service costs — things like professional services fees, embalming, transportation, flowers, and staff — is more limited. For most states, this exclusion applies only to the Medicaid applicant and their spouse. It does not extend to other family members in the same way the burial space exclusion does.

This means the irrevocable funeral trust strategy covers the applicant’s own funeral service costs, but purchasing a similar arrangement for an adult child or sibling under the same Medicaid-planning rationale won’t necessarily receive the same treatment. Check your state’s rules carefully.

State-by-State Variations You Must Verify

Federal Medicaid law sets the framework, but states have considerable discretion in implementing the rules. The variations are significant enough that what works cleanly in one state may be unavailable or structured differently in another.

States That Don’t Allow Standard Irrevocable Funeral Trusts

Michigan and New York are the two notable exceptions. These states do not permit the use of standard irrevocable funeral trusts for Medicaid spend-down purposes in the typical way. However, both states allow irrevocable prepaid funeral contracts purchased directly from a funeral home. If you’re in Michigan or New York, the contract is made with the funeral home itself rather than through a separate trust structure. The effect for Medicaid purposes is similar, but the mechanism — and the fine print — differs.

States with Dollar Caps on Irrevocable Funeral Trusts

Approximately half of the states impose a maximum dollar limit on the amount that can be placed into an irrevocable funeral trust and still be excluded from Medicaid assets. These caps vary widely — some states set them at $5,000, others at $10,000 or $15,000, and a few impose no cap at all. Funding beyond the cap may count as a countable asset.

This is one of the most critical details to verify with an elder law attorney in your state before funding a contract, especially if you’re planning for a traditional burial, which can easily run $10,000–$15,000 or more.

For state-specific preneed regulations and consumer protections, visit your local guide. We explore statutes affecting preneed contracts in all 50 states.

Medicaid Rules for Married Couples

The rules above apply primarily to a single applicant. For married couples, Medicaid’s spousal impoverishment protections add another layer of planning opportunity.

When one spouse applies for Medicaid (the “institutionalized spouse”), the other (the “community spouse”) is generally allowed to retain a significantly higher asset allowance — known as the Community Spouse Resource Allowance (CSRA). The exact amount varies by state but is typically between $30,000 and $150,000 in 2024.

Within this framework, a married couple may be able to fund irrevocable preneed contracts for both spouses and have both excluded from the Medicaid asset calculation — provided each contract is properly structured under state rules. The burial space exclusion for immediate family members, described above, also opens additional planning options for couples with adult children.

Spousal Medicaid planning is complex and highly state-specific. An elder law attorney is particularly important here, as the wrong strategy can accelerate Medicaid disqualification rather than protect against it.

The Look-Back Period: What You Need to Know

Medicaid has a five-year look-back period for asset transfers. If you transfer assets — give money away, sell property below market value, or make gifts — within the five years before applying for Medicaid, those transfers can result in a penalty period during which Medicaid will not pay for care.

Funding an irrevocable preneed funeral trust is not considered a disqualifying transfer under Medicaid rules, because you’re purchasing a specific item of equivalent value (funeral services), not simply giving money away. This is one reason why the irrevocable preneed contract is recognized as a Medicaid planning tool rather than a prohibited asset transfer.

However, this protection depends on the contract being genuinely irrevocable and properly structured. A contract that allows cancellation and refund — even a partial one — may not receive the same treatment. Again, the terms of the specific contract matter.

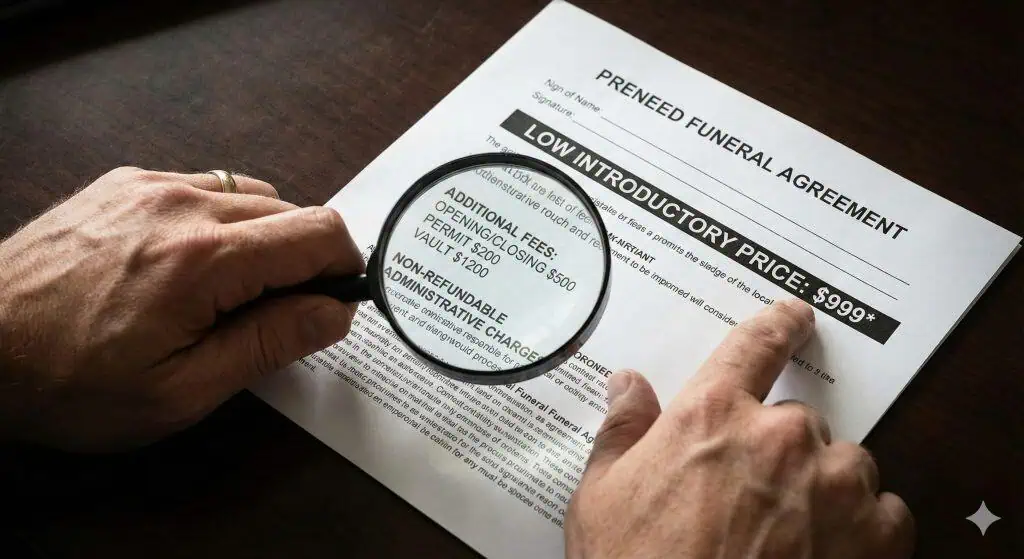

Red Flags to Watch For When Buying for Medicaid Planning Purposes

Unfortunately, the preneed funeral industry has a documented history of fraud and mismanagement. When you’re buying a preneed contract specifically for Medicaid planning, the stakes are higher than usual, because a poorly structured contract may not only expose you to financial risk — it may fail to achieve the Medicaid exclusion you planned for.

🚩 Watch for these warning signs:

- The contract is described as “irrevocable” but contains a cancellation provision. A genuinely irrevocable contract should not allow you to retrieve funds under any circumstances. If there’s a refund clause, it may not qualify for Medicaid exclusion.

- The funeral provider cannot tell you what percentage of your payment goes into trust. Many states require a specific percentage (often 80–100%) to be held in a state-regulated trust. If the provider can’t answer this question clearly, that’s a serious problem.

- The contract doesn’t name the state Medicaid agency as the residual beneficiary. In states that require this, a contract without that designation may not qualify for the Medicaid asset exclusion.

- The provider is not licensed to sell preneed contracts. Preneed sales require a specific license in most states. Ask to see their license and verify it with your state’s funeral regulatory board.

- There are blank spaces in the contract. Never sign a preneed contract with any fields left blank. Spaces can be filled in after the fact without your knowledge or consent.

- The provider pressures you to sign quickly. Legitimate preneed planning is not time-sensitive. Any high-pressure sales tactic is a red flag.

Under the FTC Funeral Rule, all funeral providers are required to give you an itemized General Price List when you inquire about services. Request it at the start of any conversation, not the end.

Alternatives to an Irrevocable Preneed Contract for Medicaid Planning

An irrevocable preneed contract is not the only way to set aside funds for funeral costs in a Medicaid context. Depending on your state and situation, you may have other options.

Payable-on-Death (POD) Account / Totten Trust

A POD account designates a beneficiary who can access the funds after your death without going through probate. However, a standard POD account is revocable — you can withdraw the funds at any time — so Medicaid will count it as a countable asset. A POD account is a useful estate planning tool in many contexts, but it generally doesn’t serve the Medicaid spend-down purpose that an irrevocable contract does.

Final Expense (Burial) Insurance

A burial insurance policy pays a death benefit to your family, who then pays the funeral provider directly. Some burial insurance policies may be treated as exempt under Medicaid rules if the face value is below your state’s threshold (often $1,500), but policies above that threshold may be counted as an asset at their cash surrender value. The rules vary considerably by state.

Direct Purchase of Burial Spaces

As noted above, the unlimited burial space exclusion is a standalone planning option that doesn’t require an irrevocable preneed contract. If your primary concern is protecting cemetery plot costs, purchasing those separately — outside of a funeral trust — may be a simpler path.

Each of these options has different implications for Medicaid eligibility, estate planning, and tax purposes. A financial advisor with experience in elder law or a qualified elder law attorney can help you evaluate which combination makes sense for your situation.

Making the Right Decision For You

A preneed funeral contract structured as an irrevocable trust can be a powerful and legitimate Medicaid planning tool — but only when the contract is properly drawn, the correct beneficiary is named, state dollar caps are respected, and you’ve verified the provider is licensed and reputable.

The single most important step you can take before signing anything is to consult a qualified elder law attorney in your state. Medicaid rules change, state-specific variations are significant, and the difference between a contract that achieves your planning goals and one that doesn’t often comes down to a few clauses buried in the fine print.

For more on the consumer protections that apply to all preneed contracts — regardless of Medicaid planning — visit our full guide to Planning a Funeral in Advance.

To find out what state laws govern preneed sales and consumer protections in your state, visit our State Guide to Funeral Laws.

How Funeral Pre-Planning Protects Families

Funeral pre-planning offers several benefits for families navigating Medicaid eligibility and long-term care planning.

Planning ahead allows individuals to:

- Ensure funeral expenses are covered in advance

- Reduce financial stress on surviving family members

- Document personal wishes for burial or cremation

- Avoid rushed decisions during a time of grief

- Legally reduce countable assets for Medicaid eligibility

Pre-planning also gives families time to compare funeral providers and select arrangements that best reflect their wishes and financial priorities.

Affordable Cremation Planning Options

Many families today choose direct cremation when planning cremation arrangements in advance. Direct cremation is typically the most affordable funeral option and allows families to hold a memorial service later. The DFS Memorials coalition of local, independent funeral providers all serve to offer affordable cremation plans ~ prices start from $795. Click below to check a price near you today.

Direct cremation generally includes:

- Transportation of the deceased

- Basic care and preparation

- Required legal paperwork and permits

- The cremation process

- Return of the cremated remains to the family

Families can then arrange a memorial service or celebration of life at a time and location that is meaningful to them, without the costs associated with a traditional funeral service.

Because cremation costs can vary widely, comparing providers and understanding available options are important parts of funeral pre-planning.

Featured Guides on Funeral Pre-Planning

Final Thoughts on Preneed Funeral Contracts & Medicaid

Medicaid funeral planning is an important but often misunderstood aspect of long-term care preparation. By understanding how funeral trusts, burial allowances, and prepaid funeral arrangements affect Medicaid eligibility, families can make informed decisions that protect both their financial resources and their funeral wishes.

Planning ahead not only helps ensure funeral expenses are covered but also provides peace of mind, knowing loved ones will not face difficult financial decisions during an already emotional time.

Families considering funeral pre-planning should review their state’s Medicaid rules carefully and seek guidance from qualified professionals when necessary.

Frequently Asked Questions

An irrevocable preneed funeral contract is generally not counted as a countable asset for Medicaid eligibility purposes. A revocable contract — one you can cancel and receive a refund from — is counted as an asset. The distinction between revocable and irrevocable is the key factor.

The burial space exclusion (cemetery plots, urns, niches, crypts) extends to immediate family members with no dollar cap. However, the funeral service cost exclusion generally applies only to the Medicaid applicant and their spouse, not to other family members. Check your state’s rules before funding contracts for other relatives.

In most states, any funds remaining after funeral costs are paid go back to the state Medicaid program as part of Medicaid estate recovery. This is a requirement in states that allow irrevocable funeral trusts for Medicaid spend-down purposes, because those funds were excluded from your assets on the condition that the state can recover them.

No. Funding an irrevocable preneed funeral contract is not treated as a disqualifying asset transfer under Medicaid’s five-year look-back period, because you’re purchasing something of equivalent value rather than giving money away. However, the contract must be genuinely irrevocable to receive this treatment.

It depends on your state. Approximately half of US states impose a dollar cap on the amount that can be placed in an irrevocable funeral trust and excluded from Medicaid asset limits. Caps vary widely — from around $5,000 to $15,000 or no cap at all. Funding above the cap may count as a countable asset.

Yes — this is strongly advisable. Medicaid rules are state-specific, change over time, and the wrong contract structure can fail to achieve the planning goal you intended. A qualified elder law attorney can review the contract terms, confirm your state’s requirements, and help you structure the arrangement correctly.

What happens will depend on the contract you signed. A transferable funeral plan will allow you to move your arrangements to another provider – without any penalty. It is important to check your preneed plan IS transferable before you commit.